Impact of Venezuela, Iran, and the Eastern Mediterranean on Oil & Gas

Overview

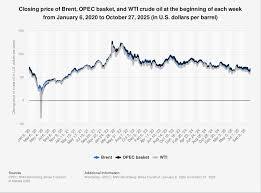

As January 2026 concludes, global oil and gas markets appear stable on the surface, with Brent crude trading in a narrow $56–$64 per barrel range. This price stability, however, masks a profound structural shift in the global energy system. According to the document, the world is experiencing one of the highest levels of geopolitical risk in decades, yet prices are being artificially restrained by a structural oversupply of oil—what the IEA terms a “bloated balance.”

Three interconnected geopolitical theaters are reshaping energy security:

Direct U.S. military intervention in Venezuela

Escalating economic warfare against Iran

Militarization of gas infrastructure in the Eastern Mediterranean

Together, these crises signal a transition away from efficiency-driven energy markets toward security-first, redundancy-heavy systems.

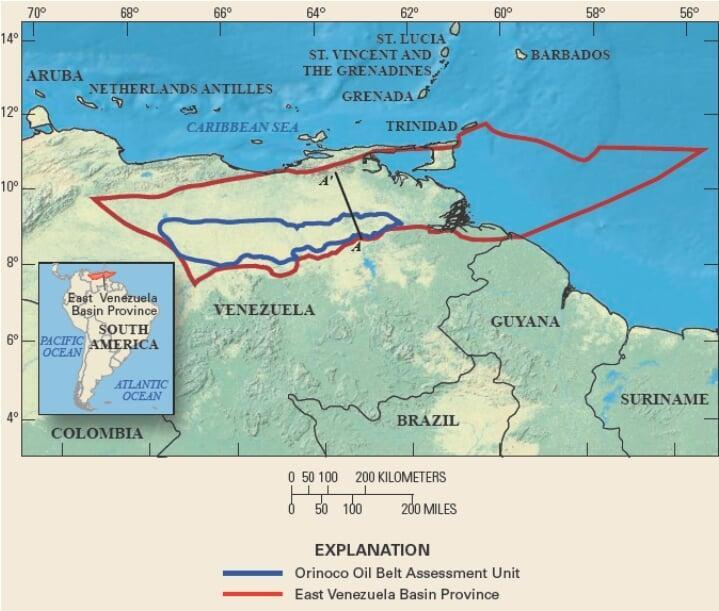

Venezuela: The End of Conventional Resource Sovereignty

Military Intervention and Governance Breakdown

The January 2026 U.S. intervention in Venezuela marks an unprecedented escalation: direct military action followed by administrative oversight of a sovereign oil sector. The operation dismantled the Maduro regime under a law-enforcement narrative, but the post-operation messaging explicitly linked regime removal to opening Venezuela’s oil sector to U.S. companies.

This has created a dual-power system:

A nominal interim Venezuelan government

De facto U.S. oversight over strategic oil decisions

For global investors, this ambiguity has frozen capital deployment and raised legal uncertainty to extreme levels.

A nominal interim Venezuelan government

De facto U.S. oversight over strategic oil decisions

Maritime Blockade and Export Collapse

A U.S.-enforced maritime blockade has dismantled Venezuela’s shadow oil trade.

Key impacts include:

Export collapse from ~880,000 bpd to 300,000–500,000 bpd

Storage saturation forcing production shut-ins

Long-term damage risk to heavy crude wells in the Orinoco Belt

While effective geopolitically, the blockade has structurally damaged Venezuela’s near-term production capacity.

Oil Sector Liberalization Under Duress

To attract foreign capital, Venezuela introduced sweeping reforms:

Elimination of mandatory PDVSA majority ownership

Full operational autonomy for private operators

Offshore retention of export revenues

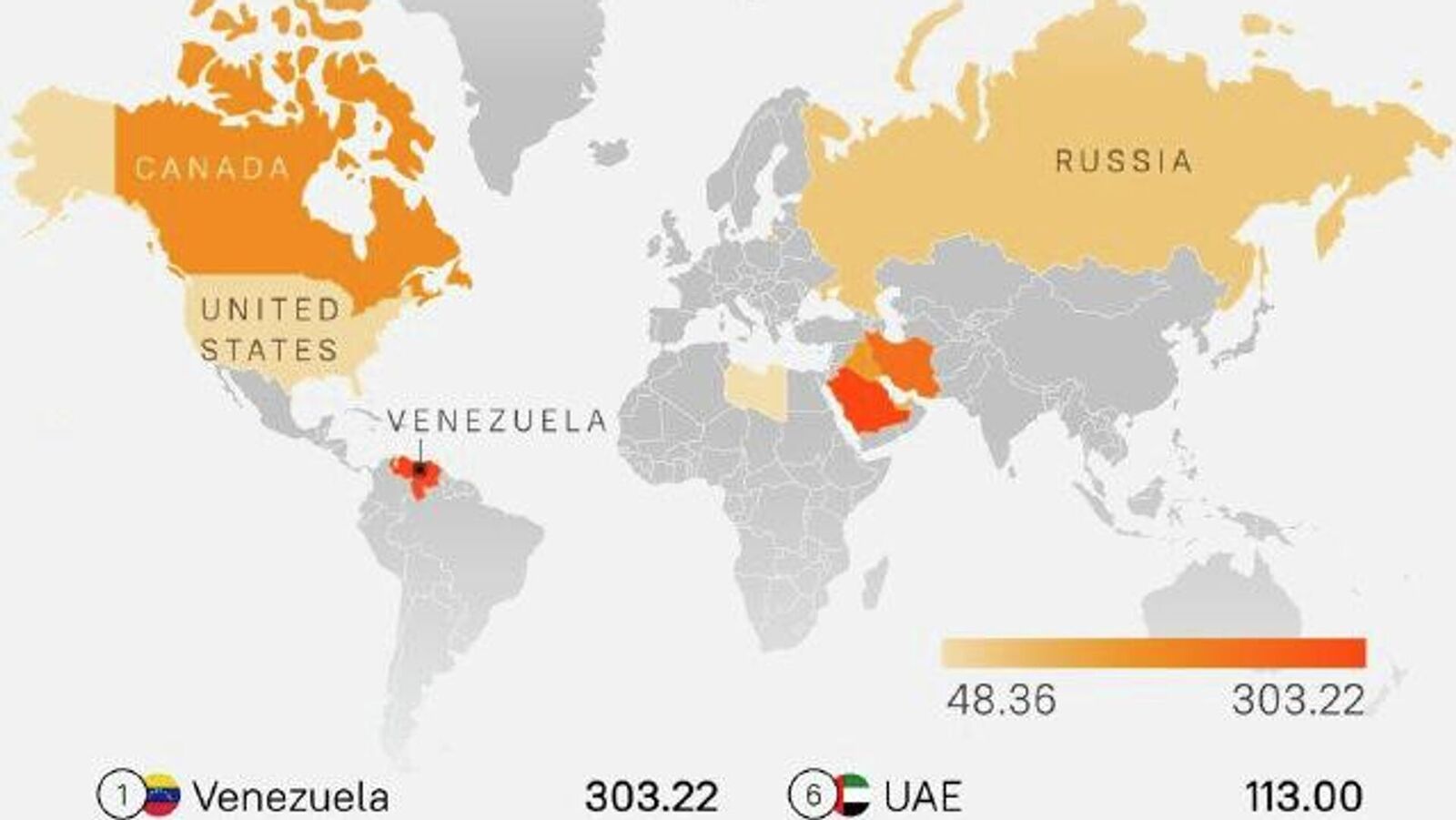

China’s Strategic Setback

China faces:

- $10–12 billion in disrupted oil-backed loans

- Loss of ~470,000 bpd of heavy crude

Increased reliance on Middle Eastern supplies

Venezuela’s collapse thus becomes a secondary shock to China’s energy security at a time of rising Middle East risk.

Iran: From Kinetic Conflict to Economic Strangulation

Post-Strike Reality

Following the destruction of Iran’s nuclear infrastructure in 2025, Tehran has pivoted from escalation to survival. While nuclear breakout risk is neutralized, economic pressure has intensified.Following the destruction of Iran’s nuclear infrastructure in 2025, Tehran has pivoted from escalation to survival. While nuclear breakout risk is neutralized, economic pressure has intensified.

The 25% Tariff Weapon

The U.S. imposed a 25% tariff on any country trading with Iran, directly targeting China.

Consequences include:

Energy trade has effectively become a tool of great-power economic warfare.

~350,000 bpd decline in Iranian exports

Elevated risk of a U.S.–China trade confrontation

Structural revenue compression for Tehran

Energy trade has effectively become a tool of great-power economic warfare.

The U.S. imposed a 25% tariff on any country trading with Iran, directly targeting China.

Consequences include:

Energy trade has effectively become a tool of great-power economic warfare.

~350,000 bpd decline in Iranian exports

Elevated risk of a U.S.–China trade confrontation

Structural revenue compression for Tehran

Dark Fleet Resilience

Iran continues exporting oil using:

Shadow tankers

Shadow tankers

Ship-to-ship transfers in Southeast Asia

Heavy price discounts

However, Iran’s own budget assumptions confirm that sanctions have capped long-term revenue potential, locking the economy into constrained growth.

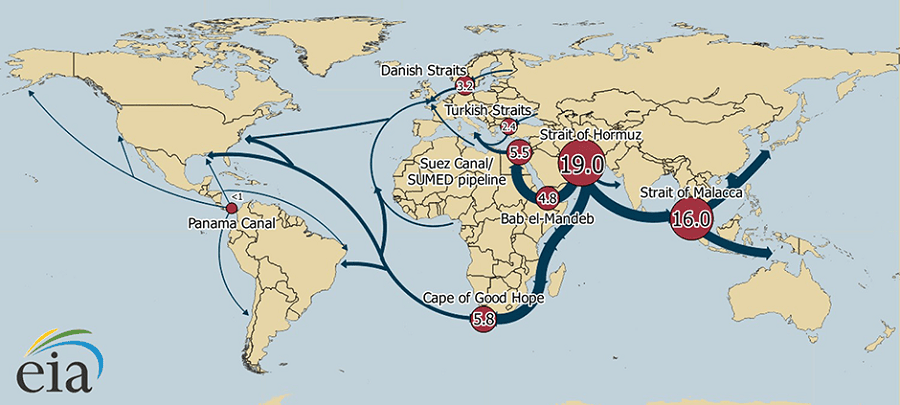

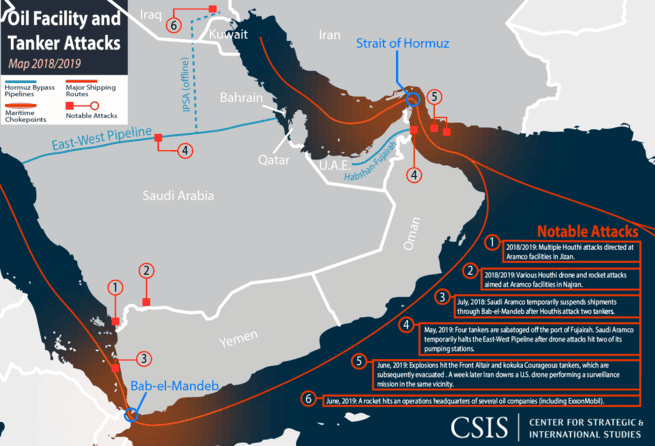

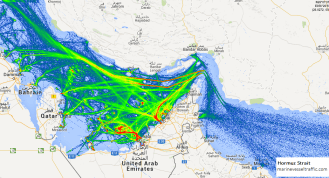

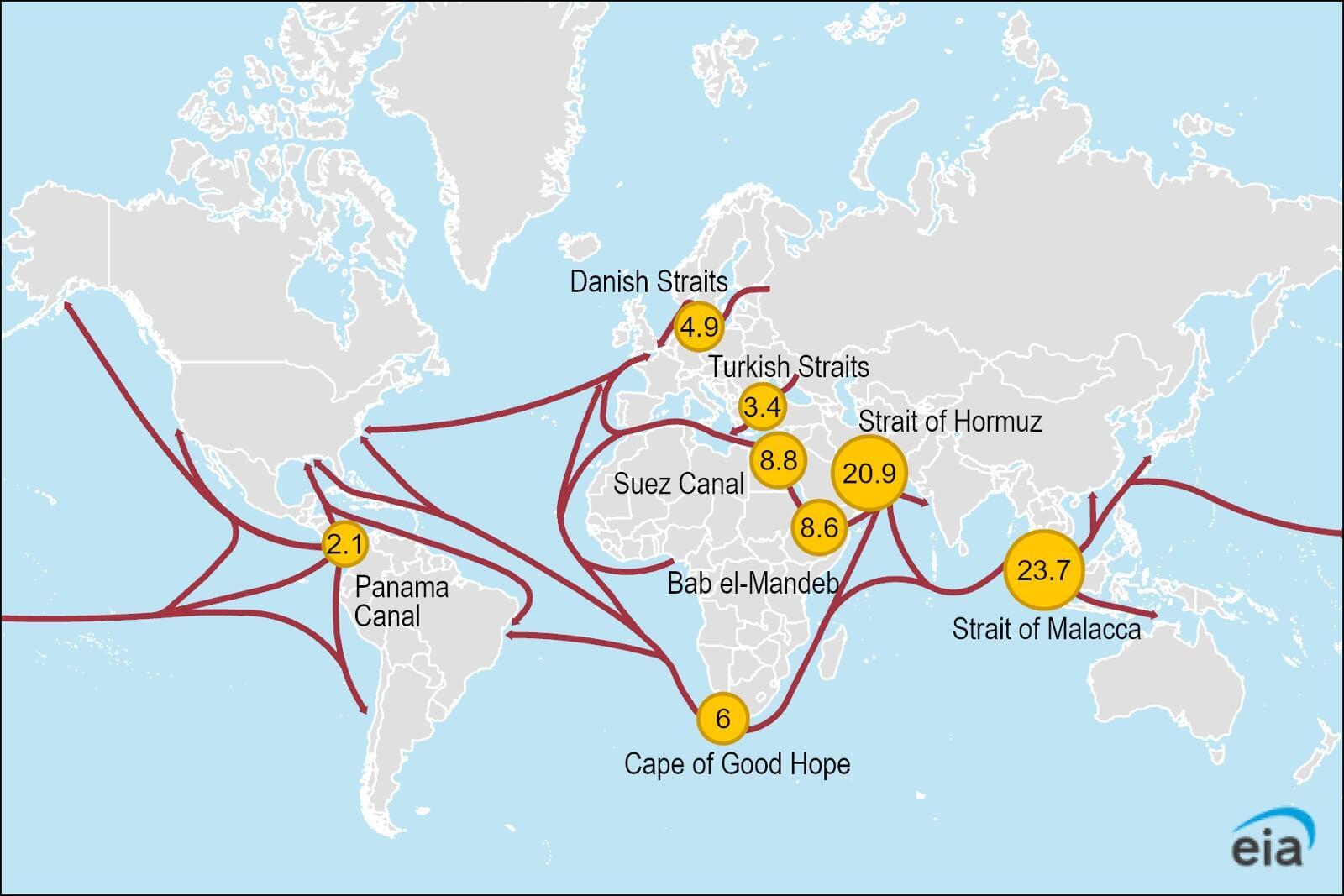

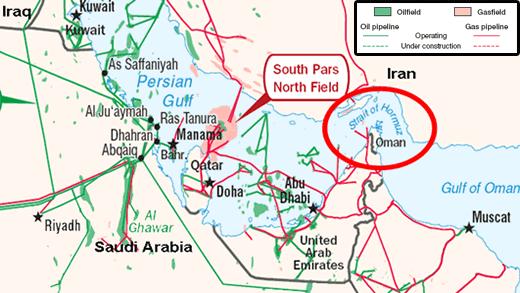

Strait of Hormuz: The Ultimate Pressure Point

The Strait of Hormuz remains the single most dangerous escalation vector. Gulf states have actively discouraged further U.S. strikes, fearing retaliation against critical energy infrastructure.

Iran instead relies on:

Cyber attacks

Vessel harassment

Gray-zone maritime tactics

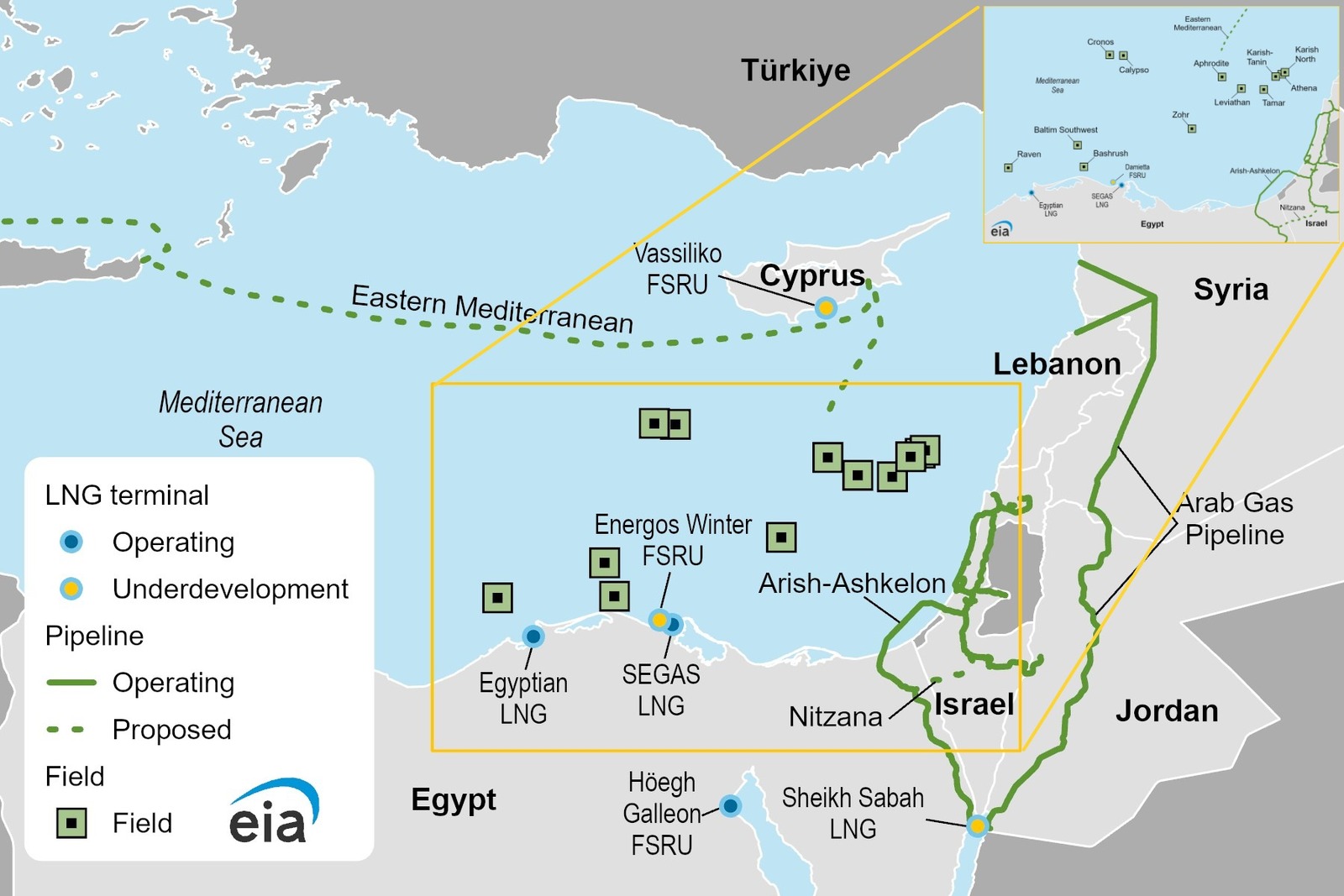

Eastern Mediterranean: Energy Assets in a War Zone

The war involving Israel, Hamas, and Hezbollah has transformed the Eastern Mediterranean gas basin into a militarized energy zone.

Key dynamics:

Offshore rigs operate under constant drone and missile threats

Naval protection has become permanent

Production continuity is treated as a national security priority

Infrastructure Expansion Despite War

Rather than retreat, operators approved major investments to expand production capacity, reinforcing the idea that energy security now depends on redundancy, not peace.

Infrastructure and LNG: The Quiet Game-Changer

One of the most consequential developments lies in infrastructure approvals, particularly for liquefied natural gas and crude exports.

Key signals include:

Restarting approvals for LNG export licenses previously stuck in regulatory limbo

Greenlighting deep-water crude export terminals capable of handling very large crude carriers (VLCCs)

Streamlining federal permitting for midstream projects

These changes matter far beyond US borders. Expanded LNG capacity directly affects Europe and Asia, where energy security and price stability increasingly depend on American supply.

For import-dependent regions, faster US export growth could translate into:

Lower volatility in gas prices

Reduced reliance on geopolitically sensitive suppliers

Stronger competition in global LNG markets

Tariffs Take Center Stage

Maritime Chokepoints and Shipping Risk

The Red Sea crisis continues to distort global energy logistics:

Western-linked vessels divert around Africa

Transit times increase by up to two weeks

Effective tanker capacity shrinks

Insurance markets now function as de facto regulators of global trade routes.

Why Prices Haven’t Exploded

Despite extreme geopolitical stress, prices remain subdued due to:

Weak demand growth

Rapid non-OPEC supply expansion

Aggressive production restraint by OPEC+

Non-OPEC supply growth exceeds demand growth by more than 1.5 million bpd, absorbing geopolitical shocks that would have caused price spikes in earlier decades.

Conclusion

The events of January 2026 confirm a fundamental truth:

Political alignment

Infrastructure survivability

Maritime security

Strategic redundancy

The world is transitioning from “just-in-time” energy markets to “just-in-case” systems. The current oversupply delays a crisis—but it does not eliminate it.

The global energy system is stable for now, but increasingly fragile beneath the surface.