Trump’s Return and the Energy Reset:

What the First Moves Mean for Global Markets?

In early 2025, the return of Donald Trump to the White House triggered one of the fastest policy pivots the global energy industry has seen in years. Within weeks, executive actions, regulatory reversals, and tariff announcements began reshaping expectations across oil, gas, power, and clean energy markets.

This article distills the real implications of those moves—cutting through headlines to explain how domestic policy shifts, trade actions, and international reactions may alter energy supply chains, investment behavior, and prices worldwide. The narrative is analytical, neutral, and forward-looking, designed for decision-makers rather than political audiences.

1. A Rapid Push to Expand US Energy Supply

From day one, the administration signaled a clear priority: accelerate domestic energy production and infrastructure.

The early policy package focused on:

Rolling back regulatory barriers that slowed drilling, mining, and export projects

Fast-tracking permits for pipelines, LNG terminals, and crude export facilities

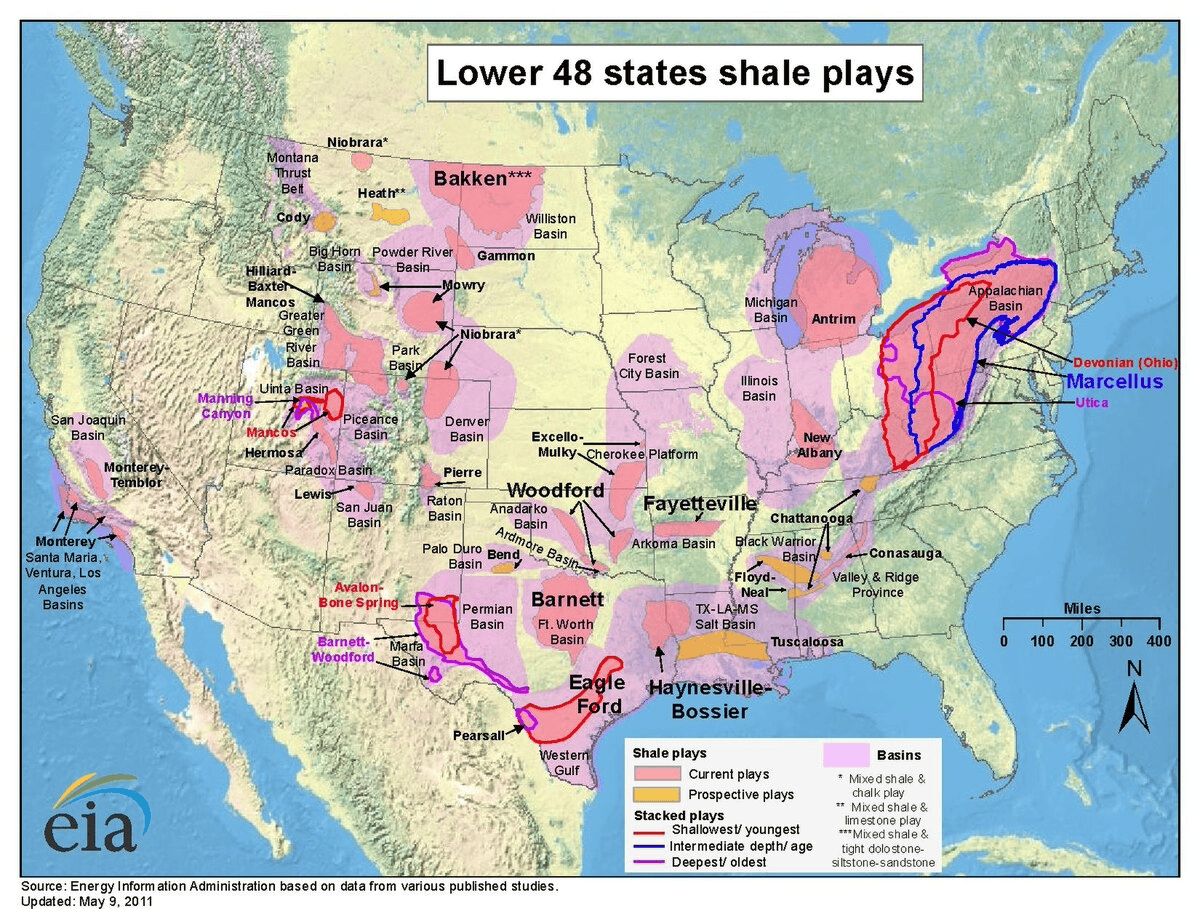

Reopening access to federal lands, with particular emphasis on Alaska and offshore resources

The intent is straightforward: increase volumes, improve logistics, and strengthen the US position as a global energy supplier. However, policy alone does not guarantee production growth. Capital discipline in shale, geological limits, and market pricing still dominate investment decisions.

Can the US Deliver a Major Production Surge?

While political rhetoric points toward dramatic output growth, market fundamentals suggest a more measured outcome. Incremental supply gains are expected, but a multi-million-barrel-per-day surge would require strong contributions from natural gas liquids and dry gas rather than crude oil alone.

In short, policy clears the runway—but markets decide how many planes actually take off.

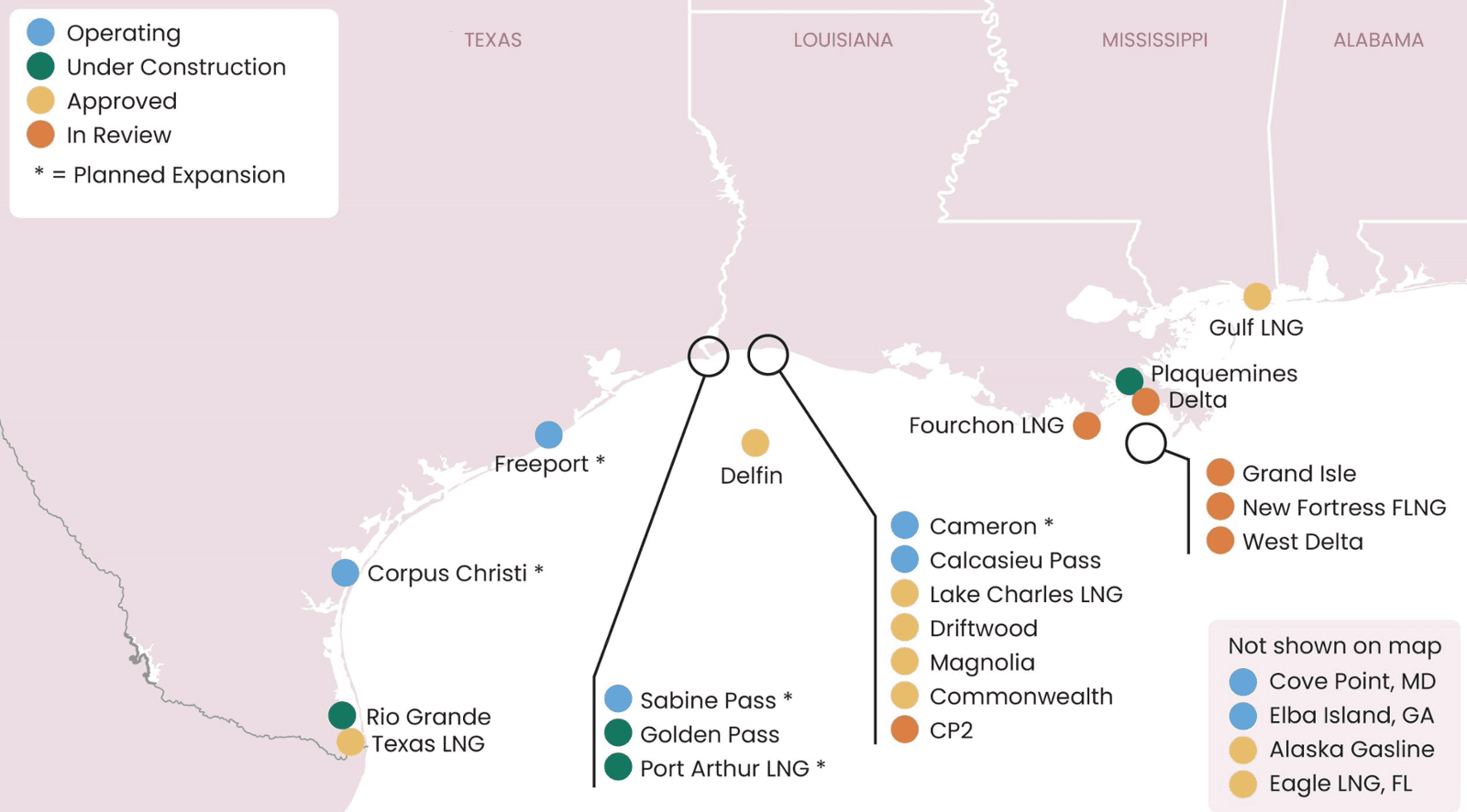

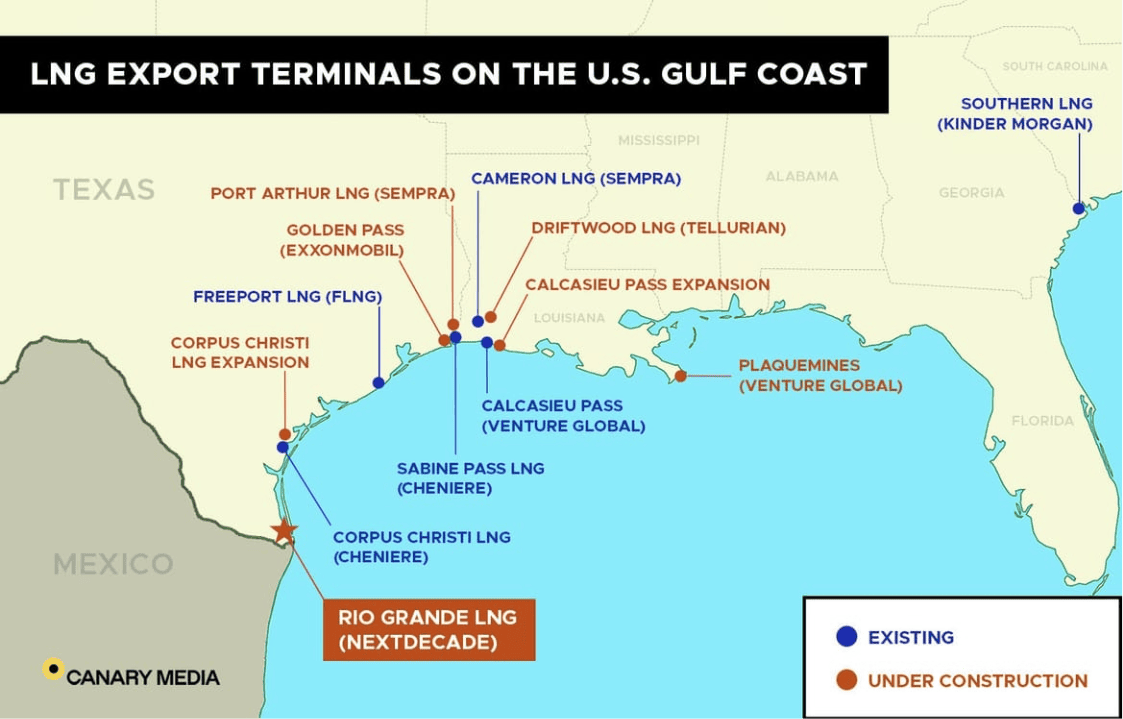

2. Infrastructure and LNG: The Quiet Game-Changer

One of the most consequential developments lies in infrastructure approvals, particularly for liquefied natural gas and crude exports.

Key signals include:

Restarting approvals for LNG export licenses previously stuck in regulatory limbo

Greenlighting deep-water crude export terminals capable of handling very large crude carriers (VLCCs)

Streamlining federal permitting for midstream projects

These changes matter far beyond US borders. Expanded LNG capacity directly affects Europe and Asia, where energy security and price stability increasingly depend on American supply.

For import-dependent regions, faster US export growth could translate into:

Lower volatility in gas prices

Reduced reliance on geopolitically sensitive suppliers

Stronger competition in global LNG markets

3. Clean Energy: Diverging Paths Within the Transition

The new policy direction does not signal a blanket retreat from clean energy—but it does reshape the hierarchy. The result is not an energy transition halt, but a more uneven and market-driven one—where affordability and scalability outweigh ideological alignment.

Likely Winners

- Solar power, driven by cost competitiveness rather than policy support

- Carbon capture and storage (CCS), backed by existing tax credits

- Blue hydrogen, benefiting from established industrial integration and incentives

Facing Headwinds

Offshore wind projects, slowed by permitting reversals

Green hydrogen, constrained by strict qualification rules and high costs

Some grid-scale storage projects exposed to imported equipment costs

4. Tariffs Take Center Stage

By February, attention shifted sharply from domestic deregulation to trade policy. New tariffs—particularly on steel, aluminum, and selected imports—introduced fresh uncertainty across energy supply chains.

Why this matters:

Steel and aluminum are foundational inputs for pipelines, rigs, power plants, and renewables

Cost inflation can delay projects even in supportive regulatory environments

Low-carbon technologies tend to be more import-dependent than traditional oil and gas

Oil and gas projects are partially insulated thanks to domestic manufacturing capacity. Clean energy projects, however, face higher exposure—especially batteries, electrolyzers, and grid equipment.

5. Canada, Mexico, and China: Uneven Exposure

Not all trading partners are equally affected by US tariff actions. This uneven exposure explains why international responses range from aggressive retaliation to cautious negotiation.

Canada and Mexico are deeply intertwined with US energy flows, particularly crude oil, refined products, and power infrastructure. Even temporary disruptions can raise costs on both sides of the border.

China, despite headline tension, has limited dependence on US crude and gas. Its vulnerability is more pronounced in petrochemical feedstocks and critical minerals.

Europe remains highly sensitive to US LNG policy due to reduced Russian imports and structural gas shortages.

6. The Bigger Picture: Policy Sets Direction, Markets Set Reality

The first months of the administration underline a critical truth: energy policy influences how markets evolve, but rarely dictates whether they do.

Deregulation may accelerate projects—but only if prices justify investment. Tariffs may protect domestic industries—but often at the cost of higher project expenses. Clean energy may lose political momentum—but economic competitiveness continues to drive deployment.

For industry participants, the strategic takeaway is clear:

Expect faster permitting and stronger export capacity in the US

Prepare for cost volatility tied to trade policy

Anticipate a more fragmented global energy transition, shaped by economics rather than uniform climate policy

Final Thought

The early energy agenda of Trump’s second term is not a simple return to the past. It is a recalibration—favoring speed, scale, and national advantage while accepting greater trade friction and market-led outcomes.

For producers, traders, investors, and policymakers worldwide, the message is unmistakable: the US energy engine is being tuned for output and leverage, and its ripple effects will extend well beyond American borders.